3Q 2025 Market Assessment: Information, Dangers, and Causes for Warning (and Optimism)

On April 2, 2025—”Liberation Day”—President Trump’s tariff plan triggered a pointy 12% drop within the S&P 500 ((SP500), (SPX)) in simply 4 buying and selling days. That shock now looks like a distant reminiscence. Since then, U.S. shares have put collectively two sturdy quarters. In 3Q, the Dow (DOW) rose 5%, the S&P 500 8%, the Nasdaq (NDAQ) 11%, and small-caps (Russell 2000) jumped 12%—their greatest quarter since 2023 and first new closing all-time excessive since 2021. By way of the tip of 3Q, the S&P 500 had set 28 all-time closing highs.

As of October 6, the S&P 500 had climbed greater than 30% over the prior six months. Historical past suggests such explosive positive aspects could also be tough to maintain: as CNBC’s Fred Imbert famous, when the S&P has superior 30%+ over a six-month interval, the index has averaged simply 3.6% returns within the following three months and 5.9% over the following six months. Even so, these figures are hardly disappointing.

The rally, nevertheless, was removed from even. An “equal-weight” model of the S&P 500—the place each firm counts the identical—rose solely 4% in 3Q. That stands in distinction to the extra usually cited model of the index, the place bigger corporations like Apple (AAPL) or Microsoft (MSFT) have an outsized influence. In apply, many of the positive aspects got here from only a handful of giants. At this time, 10 shares make up greater than 40% of the index—an unprecedented degree of focus.

The Fed, Politics, and Coverage Shifts

It is not all the time straightforward to say precisely why the inventory market strikes, however a significant driver of the market’s latest advance has been altering expectations in regards to the Federal Reserve. Traders started to imagine the Fed could be extra keen to chop rates of interest, with rising hopes for one or two extra cuts (along with the 25-bps price lower that came about in September) earlier than the tip of the yr.

The coverage debate has been something however quiet. The Trump administration has pressed the Fed to chop charges extra aggressively, even trying to take away Governor Lisa Prepare dinner—a transfer that stirred contemporary considerations in regards to the central financial institution’s independence. For now, markets are comfy ignoring this break from long-standing norms. However because the “Liberation Day” selloff reminded us, market course can reverse out of the blue, and investor confidence may shift simply as shortly.

Earnings, Shoppers, and the Actual Economic system

Company earnings for 2Q got here in forward of expectations (though this was due partly to a pull ahead in demand attributable to tariff uncertainty), and momentum doubtless carried into 3Q regardless of tariff headwinds (3Q earnings season unofficially begins in mid-October). On 2Q earnings calls, many corporations pointed to value pressures from commerce coverage but additionally highlighted measures to offset the influence.

The buyer remained resilient—a key help for the financial system—however cracks are forming. Decrease-income households are underneath seen pressure, and even higher-income households are starting to really feel pinched by larger borrowing prices and elevated costs in areas like housing and healthcare.

Winners & Losers

The 3Q positive aspects had been international, not simply confined to america. Asian markets posted double-digit positive aspects, with Japan’s Nikkei (NKY:IND)up 11.0%, Hong Kong’s Hold Seng (HSI) up 11.6%, and China’s Shanghai Composite (SHCOMP) up 12.7%. Europe lagged however nonetheless delivered a good 3.1% acquire as measured by the Stoxx Europe 600 (STOXX). Commodities informed a blended story. Gold superior 15.1% (bringing its year-to-date acquire to ~45%), whereas oil slipped lower than 1% regardless of ongoing geopolitical uncertainty, and Bitcoin (BTC-USD) gained 8%.

Throughout the U.S., enjoying protection didn’t repay, with the historically “safer” Shopper Staples sector the one S&P 500 sector to say no for the quarter, dropping nearly 3%. The most effective sectors for the quarter had been Know-how, which superior 13.0%, and Communication Providers, which gained 11.8%. By way of 3Q no sector of the S&P 500 is detrimental for the yr.

AI, Mega-Caps, and Alphabet (GOOG) (GOOGL)

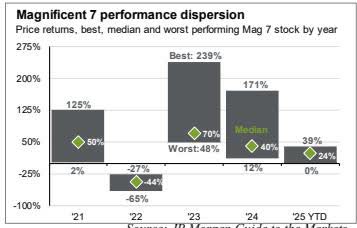

The factitious intelligence commerce confirmed no indicators of slowing, with mega-cap corporations—together with Apple, Alphabet, and NVIDIA (NVDA) —as soon as once more powering the market larger. Alphabet rebounded sharply, rising almost 40% as considerations over antitrust challenges and AI competitors eased. However not the entire so-called Magnificent Seven have confirmed equally magnificent. In 2025, efficiency dispersion throughout the group has been important, starting from a 39% acquire for NVIDIA (via 3Q) to flat returns for Amazon (AMZN), with the median inventory nonetheless advancing a market-beating 24%. Importantly, with out the contribution of the Magnificent Seven, the S&P 500 would have superior solely 11% year-to-date; the group has been answerable for roughly 45% of the index’s 14% total return. The lesson: even throughout the market’s most celebrated cohort, selectivity has mattered.

Supply: JP Morgan Information to the Markets

Are At this time’s Market Leaders Invincible?

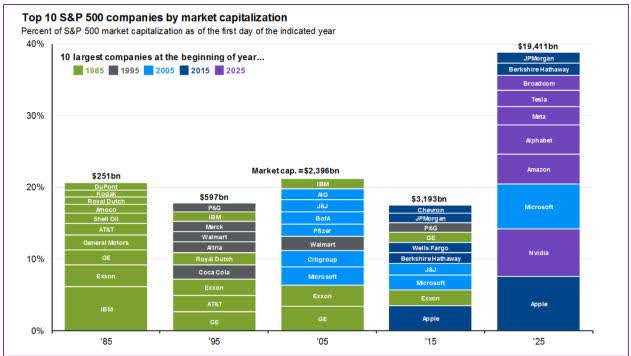

For now, the Magnificent Seven seems to be almost untouchable, buoyed by formidable benefits comparable to community results, cash-rich steadiness sheets, and large R&D budgets. But historical past exhibits that company dominance isn’t everlasting.

Trying again over the previous 5 many years, the composition of the highest 10 U.S. corporations by market capitalization has modified dramatically. Of at this time’s 10 largest corporations, solely 4 had been on the listing a decade in the past, and only one appeared 20 years in the past. No firm has remained within the high 10 for all 5 many years, and solely two—GE and Exxon (XOM)—managed to remain there for 4.

The lesson is that nothing lasts perpetually. A lot of at this time’s market leaders command lofty valuations, and whereas buyers are betting closely that their progress will proceed, historical past suggests such confidence could show misplaced.

Supply: JP Morgan Information to the Markets

Causes to Cheer, Causes to Fear

There are definitely causes to imagine the bull case for shares stays intact. Earnings progress has been sturdy, and momentum may carry into 4Q when corporations start reporting 3Q outcomes, even within the face of tariff headwinds. Potential tax cuts and deregulation could additional bolster earnings, whereas low oil costs act like a tax lower for shoppers, looming price cuts present further help, and a weaker greenback enhances the competitiveness of U.S. items overseas. Nonetheless, whereas these tailwinds are actual, historical past reminds us that markets usually stumble simply when the consensus narrative appears most convincing.

The Shopper Is Nonetheless Spending

Shopper spending progress (not adjusted for inflation) is operating at a gradual however modest tempo of round 5% year-over-year—sufficient to maintain the financial system shifting, however not sturdy sufficient to drive significant financial progress.

Whereas circumstances may change, this factors to the Fed edging nearer to an elusive comfortable touchdown, the place demand cools with out collapsing and policymakers acquire cowl to contemplate price cuts. That stated, that is removed from a fait accompli : the Fed nonetheless faces the fragile activity of reducing charges sufficient to help the labor market, however not a lot that inflation reaccelerates.

Housing Might be The Swing Issue

Housing may show to be one of many key indicators of the place the financial system goes from right here. As we’ve mentioned in earlier letters, the U.S. faces a structural housing scarcity. Estimates recommend the nation wants greater than 16 million new houses by 2033—a spot that can’t be closed with out a main pickup in building. For the previous few years, larger mortgage charges have sidelined each patrons and sellers, creating an uncommon freeze in exercise.

Might Curiosity Charges Be a Tailwind?

Whereas the Fed doesn’t instantly management the 10-year Treasury yield—the benchmark for many mortgages—its actions affect the broader price atmosphere. If mortgage charges ease, housing demand that has been locked up by larger borrowing prices could possibly be unleashed, resulting in a surge in transactions, new building, and ripple results throughout the financial system from ancillary spending on objects like furnishings, renovations, and sturdy items. This can be a actual risk.

Housing instantly accounts for about 3%–5% of GDP via residential mounted funding, and its broader affect is even bigger when you think about providers like rents and utilities.

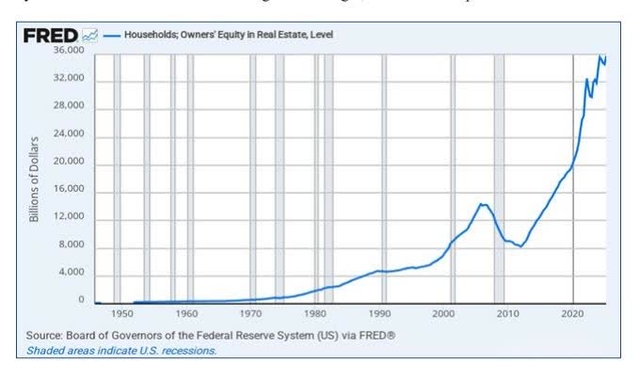

People additionally sit on substantial house fairness ($35 trillion in complete) a good portion of which could be unlocked via house fairness strains of credit score, additional stimulating consumption. On this state of affairs, the wealth impact from housing may present the financial system with one other leg up. The important thing caveat is that long-term charges don’t all the time fall in tandem with Fed coverage, as they’re additionally formed by international capital flows, inflation expectations, and monetary dynamics.

If the Fed navigates this fastidiously—and absent main exogenous shocks—housing could possibly be the catalyst that transforms a modest comfortable touchdown right into a stronger, extra sturdy growth.

However There are Dangers

All will not be excellent within the financial system or the inventory market—neither is it ever. Valuations are stretched by historic requirements: the S&P 500 trades at about 23 instances anticipated earnings, a degree reached solely twice this century. That is fairly costly in comparison with its long-term common within the mid-teens. Against this, there are nonetheless numerous good companies throughout the index buying and selling under 10 instances earnings. In the meantime, the financial system is dropping momentum—job progress is faltering, manufacturing is contracting, and housing stays weak.

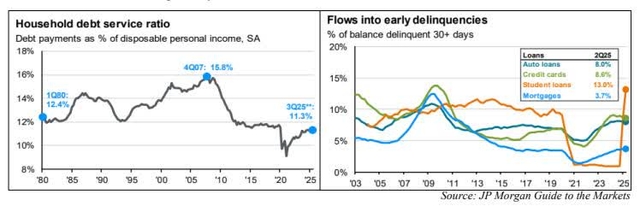

Shoppers nonetheless seem in fairly fine condition. Many have benefited from giant positive aspects in each equities and actual property and carry comparatively low debt burdens by historic requirements. But there are cracks rising. Early delinquencies are rising throughout auto loans, bank cards, pupil loans, and even mortgages a development we’re monitoring carefully.

Indicators of hypothesis are additionally arduous to disregard:

Opendoor Applied sciences (OPEN), an internet home-buying platform, has surged almost 400% this yr, at instances accounting for 13% of complete U.S. buying and selling quantity.

Greater than 90 SPACs have raised $20 billion thus far in 2025, making it the busiest yr since 2023.

New IPOs are advancing a median of 34% on their first day of buying and selling.

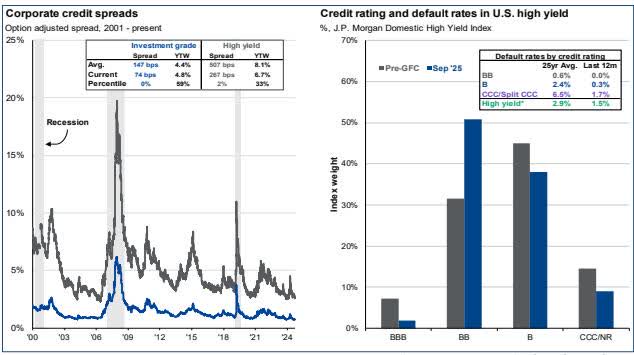

Company Credit score Has Us Anxious

Funding-grade bonds are paying solely 0.74% greater than Treasuries—the thinnest cushion since 1998. Riskier “junk” bonds yield simply 2.7% greater than Treasuries, near the lows of 2007. In different phrases, buyers are being paid a minuscule quantity to tackle the added threat of investment-grade bonds (traditionally they’ve paid a median of 1.47% over Treasuries) and little or no to tackle the a lot higher dangers of junk bonds, versus previous cycles when junk bonds usually paid 5%–6% greater than Treasuries. As Howard Marks has noticed, “the worst loans are made at the very best of instances.”

At present ranges, buyers in each investment-grade and high-yield company credit score aren’t being adequately compensated for threat. If rates of interest rise greater than anticipated or financial progress stalls, holders of those bonds may face substantial losses. For these looking for mounted earnings publicity, we might stay cautious exterior of U.S. Treasuries.

Supply: JP Morgan Information to the Markets

Jamie Dimon’s Warning

JPMorgan (JPM) CEO Jamie Dimon lately struck a extra cautious tone than many, as Martin Baccardax of CNBC reported. He warned that markets could also be underestimating dangers tied to the administration’s strain on Fed independence, a weaker greenback, and U.S. fiscal fragility. “The extent of uncertainty ought to be larger in most individuals’s minds than what I’d name regular,” he stated. “So if the market is pricing in 10%, I’d say it is extra like 30%.”

Dimon’s feedback level to actual considerations, nevertheless it’s value remembering that his monitor file on massive calls has been blended. In 2022, simply earlier than an extended bull run, he warned of an financial “hurricane” that by no means materialized. In 2023, he argued the federal funds price may attain 7% and the financial system would falter neither got here to move.

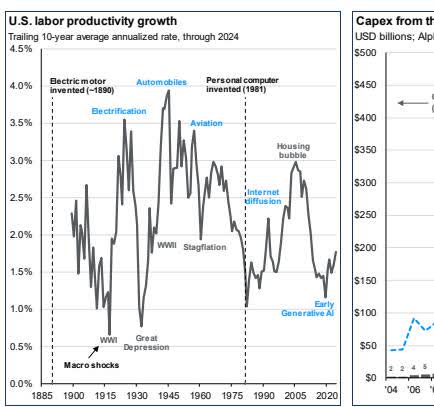

The AI Commerce and Productiveness: Transformation Takes Time

There may be little doubt that synthetic intelligence will in the end remodel the financial system. Its potential to reshape industries, improve effectivity, and create completely new enterprise fashions is actual. However buyers anticipating a direct payoff could also be upset. Historical past exhibits that main technological revolutions not often translate into instantaneous productiveness positive aspects.

Electrical energy, the inner combustion engine, and the non-public laptop all profoundly modified the world, however solely after lengthy adoption curves. Companies wanted time to reconfigure workflows, construct infrastructure, and combine new instruments. Productiveness positive aspects from innovation are likely to arrive step by step, usually after years of trial and error. AI is unlikely to be totally different.

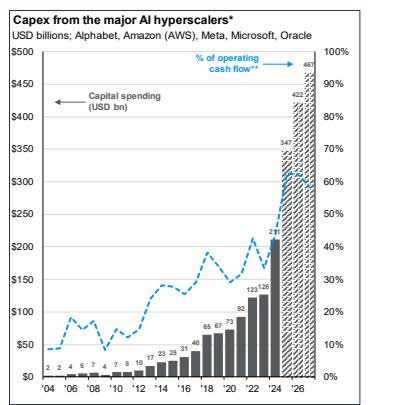

For now, AI-related spending is itself fueling the financial system. Firms are pouring billions into knowledge facilities, chips, and software program improvement. This funding wave—a lot of it with out near-term payback—has turn out to be an vital progress driver. But when enthusiasm cools or budgets tighten, the slowdown in AI capex may drag on the financial system earlier than productiveness advantages have had an opportunity to look.

Some forecasters recommend AI may ultimately usher in significant deflation, as automation reduces prices and costs throughout industries. That will be a long-term boon for shoppers. However within the close to time period, AI is inflationary, since constructing the infrastructure requires huge spending on chips, energy, and expertise. The disinflationary payoff is extra prone to come later, as soon as effectivity positive aspects unfold throughout the financial system.

The lesson is that whereas AI’s potential is big, timing issues. The expertise will doubtless change the world, simply not as shortly as many buyers hope. And till these productiveness positive aspects turn out to be actual, the financial system is leaning closely on AI-driven funding to continue to grow—help that might show extra fragile than the present investor optimism suggests.

A Phrase on Rising Markets

One of many clearest examples of risk-on sentiment in 2025 has been the outperformance of rising market equities, that are up 28% year-to-date via early October. Some could dismiss this as easy “catch-up” after a decade through which U.S. equities soared whereas EM shares gained a modest 9%. However this rally displays greater than imply reversion—a number of highly effective drivers are at work.

Key drivers of the 2025 rally:

Weakening U.S. greenback: A softer greenback makes it cheaper for rising economies to service greenback denominated debt and attracts contemporary capital inflows.

Shifting international capital flows: With developed markets dealing with excessive valuations and lingering uncertainties, buyers are looking for alternative in areas the place valuations stay compelling. The MSCI (MSCI) EM Index trades at ~14x ahead earnings versus 23x for the S&P 500.

Resilient progress and coverage reforms: A number of EM international locations have delivered strong financial progress and enacted supportive coverage measures, making them extra enticing locations for capital.

Dangers to the rally

Whereas the efficiency has been spectacular, buyers ought to be conscious of dangers. Rising markets stay extremely delicate to commodity cycles, political instability, and foreign money volatility. China, which nonetheless represents a big portion of EM indices, faces coverage uncertainty, a possible commerce conflict with america and structural financial challenges. Geopolitical tensions and capital flight dangers additionally make EM investing inherently extra unstable than developed markets.

What This Means for Rising Market Traders

Though the rally has been notable, rising markets aren’t a spot the place each investor must have publicity. Whereas the potential rewards could be important, so too are the dangers. For many buyers, a easy allocation centered totally on developed markets—with a big element in U.S. equities—is probably going essentially the most prudent path. Many buyers and monetary advisors tend to overcomplicate portfolios; in our view, simplicity is usually the higher technique. A modest allocation to EM could make sense for some, nevertheless it ought to by no means be on the expense of a well-structured, long-term core portfolio.

Backside Line

3Q underscored the market’s duality: hovering indices and resilient earnings on one hand, stretched valuations and speculative extra on the opposite. Historical past reminds us that it’s exactly in such moments when optimism feels easy—that self-discipline issues most.

At Boyar, our private-equity strategy to public markets has all the time centered on uncovering underappreciated companies with catalysts for worth realization. Whereas the headlines are dominated by a handful of mega-caps, we proceed to seek out compelling alternatives amongst missed corporations buying and selling effectively under intrinsic worth. In our expertise, it’s endurance and selectivity in these intervals of exuberance that create the very best long-term outcomes.

Finest regards,

Mark A. Boyar

Jonathan I. Boyar

IMPORTANT DISCLAIMER

Necessary Disclosures. The data herein is supplied by Boyar’s Intrinsic Worth Analysis LLC (“Boyar Analysis”) and: (A) is for common, informational functions solely; (B) will not be tailor-made to the precise funding wants of any particular particular person or entity; and (C) shouldn’t be construed as funding recommendation. Boyar Analysis doesn’t provide funding advisory providers and isn’t an funding adviser registered with the U.S. Securities and Trade Fee (“SEC”) or every other regulatory physique. Any opinion expressed herein signify present opinions of Boyar Analysis solely, and no illustration is made with respect to the accuracy, completeness or timeliness of the data herein. Boyar Analysis assumes no obligation to replace or revise such info. As well as, sure info herein has been supplied by and/or relies on third get together sources, and, though Boyar Analysis believes this info to be dependable, Boyar Analysis has not independently verified such info and isn’t answerable for third-party errors. You shouldn’t assume that any funding mentioned herein will likely be worthwhile or that any funding selections sooner or later will likely be worthwhile. Investing in securities includes threat, together with the potential lack of principal. Necessary Data: Previous efficiency doesn’t assure future outcomes. Any corporations talked about on this are for informational functions solely and the efficiency of the inventory chosen will not be indicative of the efficiency of the shares profiled in Boyar Analysis, the efficiency of the shares chosen, and the efficiency of Boyar Analysis could in truth diverge materially. This info will not be a advice, or a suggestion to promote, or a solicitation of any provide to purchase, an curiosity in any safety, together with an curiosity in any funding automobile managed or suggested by associates of Boyar Analysis. Any info that could be thought of recommendation regarding a federal tax problem will not be supposed for use, and can’t be used, for the needs of (i) avoiding penalties imposed underneath america Inside Income Code or (ii) selling, advertising and marketing or recommending to a different get together any transaction or matter mentioned herein.

")